Under Malta non-dom remittance taxation, foreign income is taxed only when remitted, while foreign capital gains remain outside the Maltese tax base.

The article explains Malta non-dom requirements, tax rules, and minimum tax obligations. It also examines how Malta non-dom status is determined and how it compares with other European non-domiciled tax regimes.

Malta non-domiciled tax regime is a remittance-basis system that applies to individuals who are tax resident in Malta but not domiciled there. The regime is governed by the Income Tax Act, in particular provisions that define taxation based on source and remittance, including Article 4(1), as well as related guidance issued by the Commissioner for Revenue[1].

Under Malta non-dom taxation:

Eligibility for Malta non-dom status depends on establishing tax residence in Malta. this usually involves spending 183 days or more in the country or maintaining a permanent home there, while the individual’s domicile of origin remains outside Malta.

The Malta non-domiciled tax regime is often used by high-net-worth individuals, entrepreneurs, investors, and remote professionals who want to avoid full worldwide taxation. It is commonly combined with residence options such as the Malta Permanent Residence Programme, which provides a legal basis to live in the country.

Malta non-dom status is determined by two separate legal concepts: tax residence and domicile. These concepts are assessed independently, but both are essential for applying Malta non-dom taxation.

The starting point is tax residence. Malta does not rely on a strict statutory 183-day rule. Instead, an individual is considered a tax resident when Malta becomes their main place of living and periods spent abroad do not interrupt this pattern.

Malta tax residence is assessed based on three key factors:

A residence permit does not automatically create Malta tax residence. Status depends on actual behaviour and connections with the country rather than immigration status. At the same time, tax residence may arise even without a residence permit if the factual criteria are met.

Domicile is a separate legal concept and reflects a person’s permanent home. It is generally more stable than tax residence and requires clear evidence to change.

Maltese law distinguishes between two types of domicile:

This intention must be supported by objective evidence, such as:

In practice, acquiring a domicile of choice in Malta is relatively difficult. Even long-term residence may not be sufficient if strong ties remain in another jurisdiction, such as a main home, active business, or close family connections. These factors may indicate that the individual does not intend to remain in Malta permanently.

As a result, many individuals who live in Malta for several years continue to be treated as non-domiciled. This status allows them to remain within the Malta non-dom regime and apply remittance basis taxation over the long term.

| Criteria | Tax residence in Malta | Domicile | Тon-dom status |

| Based on physical presence | Yes | No | Yes |

| Based on long-term intention | No | Yes | Yes |

| Requires permanent home in Malta | Often | Yes | No |

| Depends on centre of vital interests | Yes | Yes | Yes |

| Can exist without residence permit | Yes | Yes | Yes |

| Triggers Maltese taxation | Yes | No | Yes |

| Leads to worldwide taxation | No | Yes | No |

| Allows remittance basis | No | No | Yes |

Malta's non-dom regime works best where foreign income is high, Maltese-source income is limited, and remittances can be structured and controlled. It is less effective where most income arises in Malta or where another country continues to apply worldwide taxation.

How Malta's non-dom regime works. Individuals obtain residence, for example through the Malta Permanent Residence Programme, and become Malta tax residents while remaining non-domiciled. Dividends and capital gains remain in foreign accounts, while only part of the income is remitted to Malta for living expenses, for example, €50,000—100,000 per year, taxed at progressive rates up to 35%.

Why it fits. Malta non-dom remittance taxation allows foreign income to remain outside the Maltese tax base unless transferred, which can reduce overall tax exposure.

Limitations. The structure is less suitable if Maltese-source income is high or if tax residence cannot be supported by actual presence and ties.

How Malta's non-dom regime works. Eligible applicants may use the Global Residence Programme, GRP. Foreign income remitted to Malta is taxed at 15%, subject to a €15,000 minimum annual tax, while foreign income kept abroad is not taxed.

Why it fits. The structure provides predictable taxation where remittances are stable and supports internationally diversified portfolios.

Limitations. It may not apply effectively where another country continues to treat the individual as a tax resident.

GRP is generally preferable where annual remittances are high and predictable. If remittances exceed approximately €100,000 per year, a flat 15% rate may be more efficient than progressive rates under the standard Malta non-dom regime.

Where remittances are lower or irregular, the standard Malta non‑dom taxation may be more efficient, as the minimum tax may be limited to €5,000 if foreign income exceeds €35,000 and the calculated liability is lower.

How Malta's non-dom regime works. Applicants may obtain a Nomad Residence Permit. Approved remote income may be exempt for the first 12 months and taxed at 10% thereafter. If Malta tax residence is established, other foreign income may be taxed under Malta remittance basis non-domiciled rules.

To qualify for the Nomad Residence Permit, an applicant must:

Why it fits. The regime offers predictable taxation of remote income while allowing foreign investment income to remain outside Malta taxation if not remitted.

Limitations. It does not apply if services are provided to Maltese clients or if long-term residence beyond permit limits is required.

How Malta's non-dom regime works. Malta tax residence is combined with non-dom status, while wealth remains in foreign structures with sufficient economic substance. Only selected income is remitted to Malta.

Why it fits. Malta's non-domiciled tax regime offers no inheritance or estate tax, access to a wide treaty network, and no fixed annual tax, such as €100,000 or €300,000 applied in some jurisdictions. The structure can be maintained long-term while the domicile remains outside Malta.

Limitations. It may not be suitable where structures lack substance or where compliance and transparency requirements are a concern.

Malta's non-dom regime attracts internationally mobile individuals because it combines remittance-based taxation with a predictable local tax system. The framework allows foreign wealth to remain outside Malta taxation while maintaining clarity on how income is treated when brought into the country.

The advantages are primarily structural and practical rather than based only on nominal tax rates.

Under Malta non-dom taxation, foreign-source income is taxed only if it is remitted to Malta. Income that remains outside the country does not enter the Maltese tax base. This allows individuals to hold international income streams without triggering taxation in Malta by default.

Foreign capital gains arising outside Malta are not subject to Maltese tax. This rule applies even if the proceeds are transferred to Malta. This distinction is a key feature of Malta's non-domiciled tax regime and is particularly relevant for investors managing international portfolios.

Malta non-dom regime creates a clear distinction between:

This separation allows individuals to structure their finances in a way that limits exposure to full worldwide taxation.

Malta remittance basis non-domiciled system allows individuals to control when and how foreign income becomes taxable. In practice, this requires:

This flexibility is relevant for business owners, investors, and retirees who receive income from multiple jurisdictions.

Malta has 74 double tax treaties with countries including the UK, US, Canada, Australia, Singapore, Switzerland, China, UAE, and EU Member States[4].

These treaties provide:

Combined with Malta non-dom status, this network supports cross-border structuring and helps manage double taxation risks.

Malta's non-dom regime is often used alongside residence options such as the Malta Permanent Residence Programme or other permits.

For eligible individuals, residence in Malta supports travel within the Schengen Area and provides a stable base for business and personal relocation.

In addition, English is an official language used in legal and tax matters, which simplifies interaction with institutions and advisers and makes Malta practical for international structuring.

Malta does not impose inheritance or estate tax and does not apply a net wealth tax. This simplifies long-term wealth planning, particularly when assets are held outside Malta[5].

At the same time, Maltese assets, especially real estate, may be subject to stamp duty on transfer. For this reason, foreign and Maltese assets are often structured separately.

Taxation of non-domiciled residents in Malta follows specific statutory rules that determine how Maltese and foreign income is treated. The system is based on the Malta non-dom remittance taxation model, where the source of income and its movement into Malta are key factors.

Under Malta's non-dom regime, all income arising in Malta is subject to taxation, regardless of where it is received. Income tax is charged at progressive rates, which depend on the taxpayer’s personal situation.

Different tax bands apply to single individuals, married couples, and parents. Parent rates apply where an individual has custody of a child or pays maintenance. The child must be under 18, or between 18 and 23 if in full-time education. Employment status of the child does not affect eligibility[6].

| Taxpayer status | 0% | 15% | 25% | 35% |

| Single | €0—12,000 | €12,001—16,000 | €16,001—60,000 | €60,001+ |

| Married | €0—15,000 | €15,001—23,000 | €23,001—60,000 | €60,001+ |

| Parent | €0—13,000 | €13,001—17,500 | €17,501—60,000 | €60,001+ |

| Parent with 1 child | €0—15,500 | €15,501—21,200 | €21,201—60,000 | €60,001+ |

| Parent with 2+ children | €0—18,500 | €18,501—25,500 | €25,501—60,000 | €60,001+ |

Under Malta non-domiciled tax regime, foreign-source income is taxed only when it is remitted to Malta. If income remains outside the country, it is not subject to Maltese tax[7].

Foreign-source income includes:

Income is considered received in Malta when it is paid directly to the individual in Malta, or is transferred from a foreign account to Malta at a later stage.

In practice, funds brought into Malta for everyday expenses are often treated as taxable income unless it can be demonstrated that they originate from capital rather than income. Capital receipts, such as inheritance or proceeds from asset sales, are not taxed solely because they are transferred to Malta, but the source of funds must be clearly documented.

Tax treatment of capital gains depends on the location of the asset:

This distinction allows non-domiciled individuals to realise foreign investment gains and transfer proceeds to Malta without triggering local capital gains tax.

Malta non-dom taxation includes a minimum tax requirement in certain cases. If foreign income exceeds €35,000 per year and is not fully remitted to Malta, a minimum annual tax of €5,000 applies.

This rule does not replace the standard tax system but ensures a baseline level of taxation for individuals using the remittance basis.

The €5,000 minimum tax:

The minimum tax does not apply if foreign income is below €35,000 per year. For married couples, the threshold is based on combined foreign income, and the minimum applies to the couple as a whole.

In some cases, an individual may choose to be taxed on a worldwide basis instead of the remittance basis if this results in a lower overall tax liability than applying the €5,000 minimum.

Non-domiciled tax residents in Malta must comply with a set of filing, record-keeping, and reporting obligations. These requirements are defined by Maltese tax legislation and international transparency standards.

Individuals who are subject to tax in Malta, or who receive a filing notice, are required to submit an annual income tax return.

The return must include:

Deadlines are set by the Commissioner for Revenue. As a general rule, paper returns are due by June 30th, while electronic submissions may have extended deadlines[8].

Taxpayers in Malta are required to retain documentation that supports the information declared in their tax returns. Records must be kept for at least 6 years[9].

The documentation should confirm:

There is no fixed list of required documents. However, records must be sufficient to support the reported tax position if reviewed by the authorities.

Individuals recognised as tax residents in Malta may apply for a Tax Residence Certificate issued by the Commissioner for Revenue.

This document is typically used to:

Tax residence is determined based on factual circumstances, including presence and economic ties. The authorities may request supporting documents and confirmation that tax obligations in Malta have been met.

Malta participates in international information exchange systems, including the OECD Common Reporting Standard and FATCA with the United States[10].

Under these frameworks, Maltese financial institutions are required to:

Individuals do not submit CRS or FATCA reports directly. However, they must provide accurate tax residency information to banks and other financial institutions when requested.

Malta offers several residence programmes for non-EU nationals who want to establish tax residency and potentially use non-dom regime. Each option differs in cost, duration, and tax treatment.

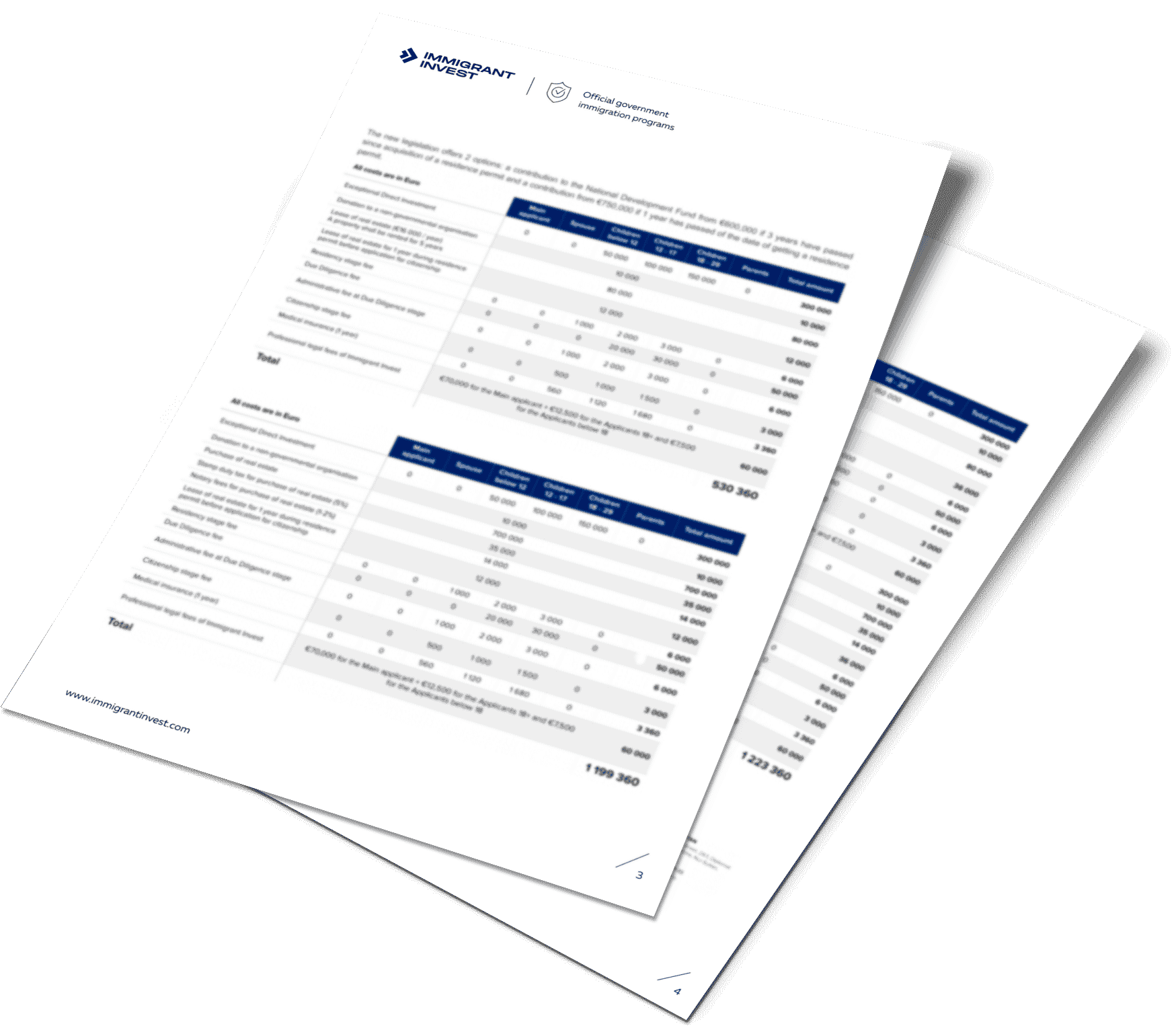

The Malta Permanent Residence Programme is designed for investors seeking long-term residence and family inclusion. It grants lifelong residence status in Malta.

Applicants must secure housing in Malta:

Additional requirements include:

Total costs start at about €169,000 for rent and €474,000 for purchase.

Permanent residence is granted without a time limit, with renewal of the residence card every 5 years. Family members may be included in one application. Among them: spouse, children under 29, and parents or grandparents.

MPRP does not provide tax benefits directly. However, if the holder becomes a Malta tax resident and remains non-domiciled, Malta non-dom taxation may apply.

The Nomad Residence Permit is intended for remote professionals earning income abroad. Applicants must have a minimum annual income of €42,000 and work for foreign employers, businesses, or clients. Work involving Maltese entities is not eligible.

The permit is issued for 1 year and may be renewed up to a total of 4 years. Key conditions include:

The main applicant can include a spouse and children in the residence application. Children over 18 must be unmarried and financially dependent.

For tax purposes, qualifying remote income may be exempt during the first 12 months. After that, it is taxed at a flat rate of 10%[11]. If the individual later becomes a Malta tax resident and remains non-domiciled, Malta non-dom remittance taxation may apply to other foreign income.

The Malta Global Residence Programme is designed for individuals seeking tax residency under a structured tax regime.

Applicants must secure accommodation:

An administrative fee of €6,000 applies, reduced to €5,500 in certain regions. Minimal costs are around €34,150 for rental and €270,200 for purchase.

The residence permit is issued for 1 year and usually renewed every 2 years. To maintain status, the individual must not spend more than 183 days per year in another country.

Family members, including spouse, children, parents, grandparents, and in some cases siblings, may be included.

The GRP operates under a separate tax regime[12]:

This programme does not rely on standard Malta non-dom rules but may serve a similar purpose for individuals with higher and more predictable remittances.

Malta non-dom status is not granted through a separate application or permit. It arises as a legal consequence of an individual’s position under Maltese tax law. The regime applies when a person becomes tax resident in Malta while retaining a domicile outside the country, and the remittance basis rules are applied accordingly.

There is no formal approval process for Malta non-dom status. Instead, the tax position depends on factual circumstances and how income is reported.

A residence permit provides the right to stay in Malta and makes it possible to establish presence in the country. While immigration status supports practical relocation, it does not in itself create tax residence or non-dom treatment.

Tax residence in Malta is determined by actual circumstances rather than formal status. In practice, it may be established through:

Supporting evidence typically includes accommodation documents, utility bills, bank records, and travel history.

Malta non-dom regime applies only if the individual remains domiciled outside Malta. This requires showing that Malta is not intended to be a permanent home and that meaningful ties are maintained in another jurisdiction.

Although there is no formal application for non-dom status, the Commissioner for Revenue may request evidence confirming both tax residence and domicile position.

Relevant documentation may include:

These documents are typically retained and provided if requested, including when applying for a Tax Residence Certificate.

Malta non-dom taxation operates through the annual tax return. The remittance basis is applied by calculating taxable income according to statutory rules.

In practice:

For each category of income, the taxpayer must determine where it arose and whether it was received in Malta. The tax calculation is then prepared accordingly.

No separate confirmation of non-dom status is issued. The tax treatment follows from the correct application of residence, domicile, and remittance rules.

Maintaining Malta non dom status requires consistency from year to year. The individual’s circumstances must continue to support tax residence in Malta, while documentation and behaviour must not indicate an intention to establish permanent domicile in the country.

European tax regimes for new residents differ in structure. Some offer temporary exemptions on foreign income, others provide relief on specific types of income, while some apply a fixed annual tax.

Malta stands out for its remittance basis approach, which can apply long term as long as non-domiciled status is maintained.

Since April 6th, 2025, the UK has replaced its non-dom regime with the Foreign Income and Gains regime. New tax residents may benefit from a 4-year exemption on foreign income and gains if they were non-resident for the previous 10 yearsх[13].

Transitional rules include partial relief and reduced tax rates on remittances until 2028.

Compared with Malta, the UK system is time-limited. Malta's non-dom regime may continue indefinitely if domicile remains outside the country.

Cyprus non-dom status provides exemption from Special Defence Contribution on dividends and interest for up to 17 years[14]. After 17 out of 20 years of tax residence, deemed domicile rules apply, and exemptions are lost.

Compared with Malta, Cyprus offers more targeted relief, mainly for passive income.

Ireland also applies a remittance basis to non-domiciled residents. Foreign income is taxed only when remitted, with no fixed duration[15]. However, Irish tax rates are higher. The top rate is 40%, and additional charges may increase the effective burden above 50%.

Malta offers lower maximum rates of up to 35% and a more flexible long-term framework.

Italy and Greece offer flat-tax regimes for new residents:

Both regimes extend to family members and replace taxation of foreign income with a fixed annual payment.

These options are typically more suitable for high-net-worth individuals. For moderate foreign income, Malta non-dom taxation may result in lower overall tax exposure.

Malta's non-dom regime is technical and depends on facts and documentation. Errors in structuring or reporting may affect the tax outcome.

The main risk is unintentionally becoming domiciled in Malta. In this case, worldwide income becomes taxable on an arising basis.

This may happen if actions suggest a permanent move, such as relocating family, acquiring substantial property, or shifting key assets and interests to Malta.

Maintaining ties abroad and avoiding long-term commitments helps reduce this risk.

Foreign income is taxed when remitted, but indirect transfers may also be treated as remittances.

Common issues include:

Clear separation of accounts and proper documentation are essential to support the tax position.

Non-dom status in Malta does not prevent other countries from taxing the same income. Tax treaties may reduce exposure, but only if Malta is recognised as the primary tax residence. Issues may arise if strong ties remain elsewhere or time spent in Malta is insufficient.

Malta may tax profits of foreign companies even if no dividends are distributed. This applies when:

Exemptions may apply depending on profit levels and activity, but structures should be reviewed in advance[18].

Income does not need to be remitted to be reported. Financial institutions apply strict compliance checks under CRS and FATCA.

Account opening may be delayed where structures are complex or documentation is incomplete. Supporting documents typically include tax returns, ownership structures, and proof of source of funds.

The €5,000 minimum tax applies only in specific cases, where foreign income exceeds €35,000 and is not fully remitted. It does not apply to certain programmes, such as the Global Residence Programme, which has its own €15,000 minimum tax.

Malta non-dom status requires consistent compliance. Tax filings, residence status, and documentation must remain aligned year to year. Even small inconsistencies in records or declared intentions may lead to additional scrutiny and tax exposure.

Immigrant Invest is a licensed investment migration company with an office in Malta that works with residence and citizenship programmes. If you wish to fall under Malta non‑dom regime, we will help you get Maltese residency.

As part of this process, Immigrant Invest conducts preliminary Due Diligence, including AML and sanctions checks, prepares document checklists, and manages the case step‑by‑step with clear timelines. The company also coordinates biometrics and official appointments, assists with property‑related requirements, and handles communication with programme authorities and other stakeholders.

After the residence status is obtained, support continues with permit renewals, address updates, and the inclusion of family members, helping maintain compliance with programme requirements over time.

Malta non-dom regime applies to individuals who are tax residents in Malta but not domiciled there. It is based on remittance taxation: Maltese income is taxed in full, while foreign income is taxed only if it is brought into Malta. Foreign capital gains are not taxed, even if remitted.

There is no separate application. Malta non-dom status arises when two conditions are met: the individual becomes a tax resident in Malta and retains a domicile outside the country. Tax residence is based on physical presence, housing, and personal or economic ties.

Foreign income is taxed only if it is remitted to Malta. If it remains abroad, it is not subject to Maltese tax. However, Maltese-source income is always taxed at progressive rates of up to 35%.

No. Capital gains arising outside Malta are not taxed under the Malta non-dom regime, even if the proceeds are transferred to Malta. This is one of the key features of the system.

A minimum annual tax of €5,000 may apply if foreign income exceeds €35,000 and is not fully remitted to Malta. This rule ensures a baseline level of taxation but does not replace standard tax calculations.

Yes. The regime can apply indefinitely as long as the individual remains tax resident in Malta and does not acquire a domicile of choice there. In practice, this requires maintaining ties outside Malta and avoiding actions that indicate a permanent move.

Key risks include unintentionally acquiring domicile in Malta, incorrect handling of remittances, and exposure to double taxation in another country. Errors in documentation or structuring may affect the tax outcome, so ongoing compliance and clear record-keeping are essential.